ESOPs: A Practical Ownership Strategy for Founders Who Think Long-Term

Authored by Matt Waters

ESOPs tend to suffer from a branding problem. Mention one to a founder and it is often dismissed as an HR initiative or a feel-good employee benefit. In reality, an Employee Stock Ownership Plan is neither soft nor sentimental. It is a structured ownership, liquidity, and succession planning strategy that, when used correctly, can provide meaningful flexibility for long-term founders.

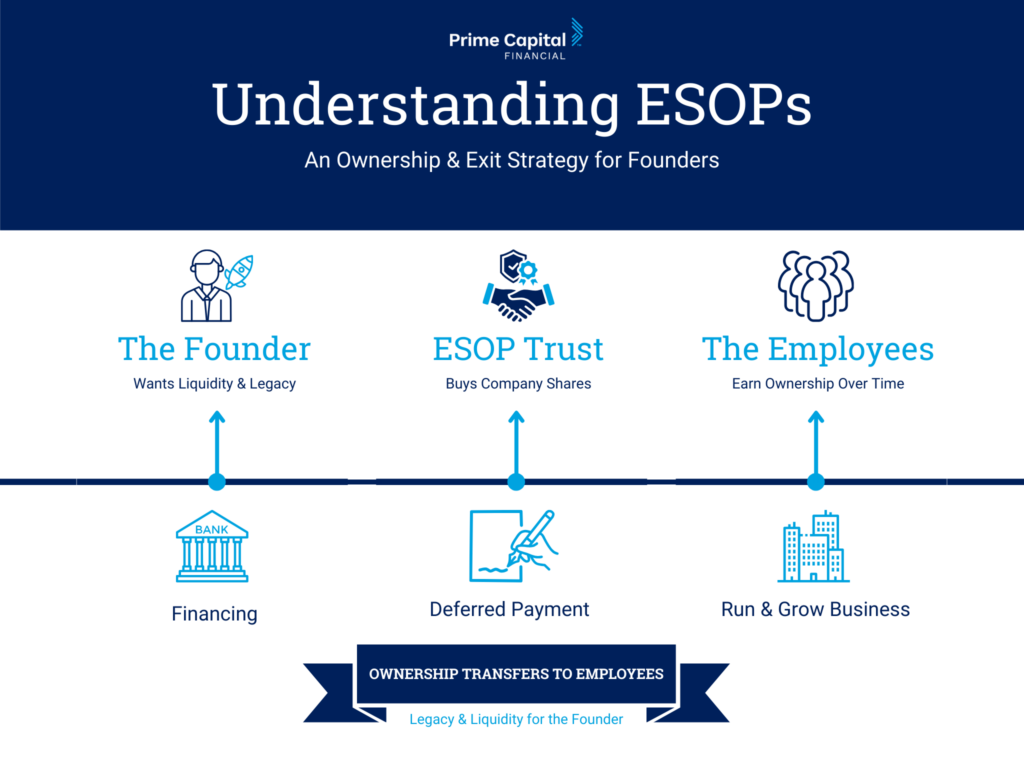

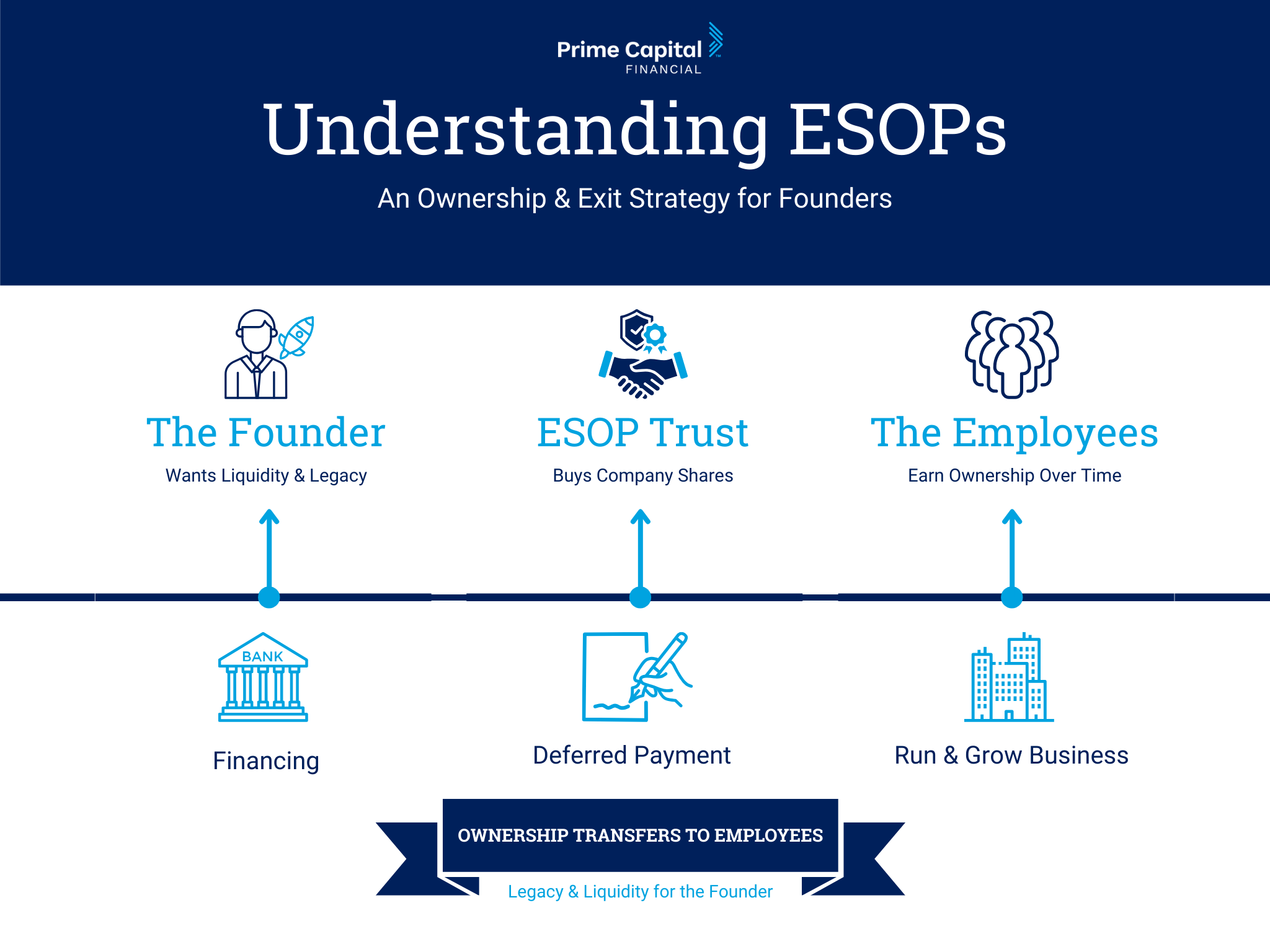

At its core, an ESOP is a qualified retirement plan that owns company stock on behalf of employees. The company establishes a trust, the trust purchases shares from the founder, and those shares are gradually allocated to employees over time. Employees do not write checks or take personal financial risk. They earn ownership through participation.

For the founder, the ESOP is simply a buyer, but one with very different incentives than private equity firms or strategic acquirers.

How an ESOP Transaction Typically Plays Out

Consider a founder-owned business valued at $50 million. It is profitable, well-managed, and generates consistent cash flow. The founder wants liquidity but has no interest in selling control, disrupting culture, or answering to outside investors.

The company establishes an ESOP and sells, for example, 40 percent of the shares for $20 million. The ESOP finances the purchase using a combination of bank debt and a seller note. Over time, the company repays that debt using future profits.

The founder receives liquidity at closing and interest payments on the seller note. The business continues operating as it always has. Employees gain a meaningful economic stake in the company’s success without assuming personal risk.

In many cases, the company’s identity, leadership team, and strategic direction remain largely intact. Ownership broadens, but control can remain exactly where the founder intends.

Control Is More Flexible Than Most Founders Expect

A common misconception about ESOP planning is that it requires surrendering control. That is rarely the case.

ESOPs can be structured as minority or majority owners. Voting control can often be retained. Boards may remain intact. Management continuity is typically encouraged rather than disrupted.

The ESOP trustee serves a fiduciary role, not an operational one. Their responsibility is to ensure fair valuation and protect employee interests. They do not run the business or dictate strategy.

For founders who value independence and long-term stewardship, this distinction is critical.

When an ESOP Makes Sense

An ESOP is generally best suited for companies with:

- Consistent profitability

- Predictable cash flow

- Strong management beyond the founder

- A desire for gradual ownership transition

It can be particularly attractive to owners who want partial liquidity today, optional liquidity later, and no external exit timeline.

For founders who care about company culture and continuity, an ESOP can offer a succession planning path that prioritizes stability. Unlike many third-party sales, ESOP structures are typically designed to support long-term continuity rather than short-term cost cutting or rapid resale.

When an ESOP Is Not the Right Fit

An ESOP is not appropriate for every business.

It may be a poor fit for companies with unstable earnings, thin margins, or founders seeking a clean and immediate exit. It is also not a strategy that should be pursued solely for tax advantages. While the tax benefits can be meaningful, they are secondary to the operational and cultural commitments required.

Like any ownership transition strategy, alignment matters more than structure alone.

How ESOP Planning Fits Into a Founder’s Wealth Strategy

From a personal wealth planning perspective, ESOP transactions can offer valuable flexibility. Liquidity generated from a partial sale may be used to diversify concentrated holdings, fund trusts, support charitable strategies, or balance inheritances among family members. Remaining ownership can be transitioned over time rather than compressed into a single decision.

This ability to separate liquidity planning from long-term succession planning is often the quiet advantage of an ESOP.

Coordinating the transaction with tax strategy, estate planning, and long-term portfolio construction is essential. Without thoughtful planning, liquidity can create complexity. When integrated properly, it can strengthen a founder’s broader financial position while preserving business continuity.

The Takeaway

An ESOP is not a compromise solution. It is a deliberate one.

For the right founder, it can provide liquidity without surrender, continuity without stagnation, and a structured path for ownership transition that aligns personal wealth goals with the long-term health of the business.

For the wrong founder, it can become an obligation rather than an opportunity.

At this level, the structure is rarely the deciding factor.

Clarity of the owner is.

Important Disclosures

The scenario mentioned in this piece is hypothetical and does not represent any clients or client experiences. This scenario was developed for educational purposes and to illustrate a potential strategy, not to guarantee a specific outcome. Your experience with our firm can and will most likely differ from what is described in this scenario.

This information does not constitute legal advice. Prime Capital Financial and its associates do not provide legal advice. Individuals should consult with an attorney regarding the applicability of this information for their situations.

Advisory products and services offered by Investment Adviser Representatives through Prime Capital Investment Advisors, LLC (“PCIA”), a federally registered investment adviser. Tax planning and preparation services are offered through Prime Capital Tax Advisory. PCIA: 6201 College Blvd., Suite 150, Overland Park, KS 66211. PCIA doing business as Prime Capital Financial | Wealth | Retirement | Wellness | Family Office | Tax Advisory.